5 Steps to a 5: AP Microeconomics 2017 (2016)

STEP 2

Determine Your Test Readiness

CHAPTER 3 Take the Diagnostic Exam

CHAPTER 3

Take the Diagnostic Exam

IN THIS CHAPTER

Summary: This chapter includes a diagnostic exam for microeconomics. It is only half the length of the real thing and is restricted to multiple-choice questions. It is intended to give you an idea of where you stand with your preparation. The questions have been written to approximate the coverage of material that you will see on the AP exam and are similar to the review questions at the end of each chapter in this book. Once you are done with the exam, check your work against the given answers, which also indicate where you can find the corresponding material in this book. Also provided is a way to convert your score to a rough AP score.

Key Ideas

![]() Practice the kind of multiple-choice questions you will be asked on the real exam.

Practice the kind of multiple-choice questions you will be asked on the real exam.

![]() Answer questions that approximate the coverage of topics on the real exam.

Answer questions that approximate the coverage of topics on the real exam.

![]() Check your work against the given answers.

Check your work against the given answers.

![]() Determine your areas of strength and weakness.

Determine your areas of strength and weakness.

![]() Earmark the pages that you must give special attention.

Earmark the pages that you must give special attention.

Diagnostic Exam: Answer Sheet

Record your responses to the exams in the spaces below.

MICROECONOMICS—SECTION I

Diagnostic Exam: AP Microeconomics

SECTION I

Time—35 Minutes

30 Questions

For the following multiple-choice questions, select the best answer choice and record your choice on the answer sheet provided.

1 . Scarcity is best defined as

(A) the difference between limited wants and limited economic resources.

(B) the difference between the total benefit of an action and the total cost of that action.

(C) the difference between unlimited wants and limited economic resources.

(D) the opportunity cost of pursuing a given course of action.

(E) the difference between the marginal benefit and marginal cost of an action.

2 . Which of the following statements is most consistent with a capitalist market economy?

(A) Economic resources are allocated according to the decisions of the central bank.

(B) Private property is fundamental to innovation, growth, and trade.

(C) A central government plans the production and distribution of goods.

(D) Most wages and prices are legally controlled.

(E) Most economic resources are owned by the government and leased to the citizens in exchange for lower taxes.

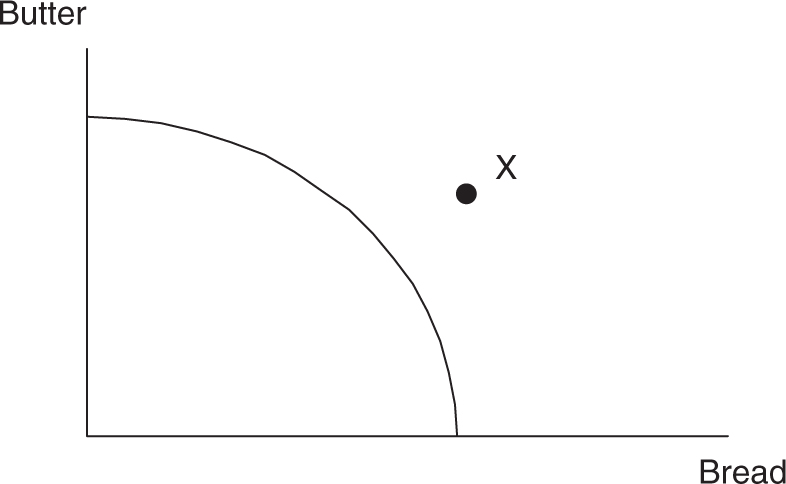

Figure D.1

3 . The graph in Figure D.1 shows a nation’s production possibility curve (PPC) for the production of bread and butter. Which of the following is true?

(A) The opportunity cost of producing more butter is a decreasing amount of bread.

(B) Point X represents unemployed economic resources.

(C) The opportunity cost of producing more butter is a constant amount of bread.

(D) Point X represents a labor force that has become less productive.

(E) The opportunity cost of producing more butter is an increasing amount of bread.

4 . Which of the following is true of equilibrium in a purely (or perfectly) competitive market for good X?

(A) A shortage of good X exists.

(B) The quantity demanded equals the quantity supplied of good X.

(C) A surplus of good X exists.

(D) The government regulates the quantity of good X produced at the market price.

(E) Deadweight loss exists.

5 . The competitive market for gasoline, a normal good, is currently in a state of equilibrium. Which of the following would most likely increase the price of gasoline?

(A) Household income falls.

(B) Technology used to produce gasoline improves.

(C) The price of subway tickets and other public transportation falls.

(D) The price of crude oil, a raw material for gasoline, rises.

(E) The price of car insurance rises.

6 . If the demand for grapes increases simultaneously with an increase in the supply of grapes, we can say that

(A) equilibrium quantity rises, but the price change is ambiguous.

(B) equilibrium quantity falls, but the price change is ambiguous.

(C) equilibrium quantity rises, and the price rises.

(D) equilibrium quantity falls, and the price falls.

(E) the quantity change is ambiguous, but the equilibrium price rises.

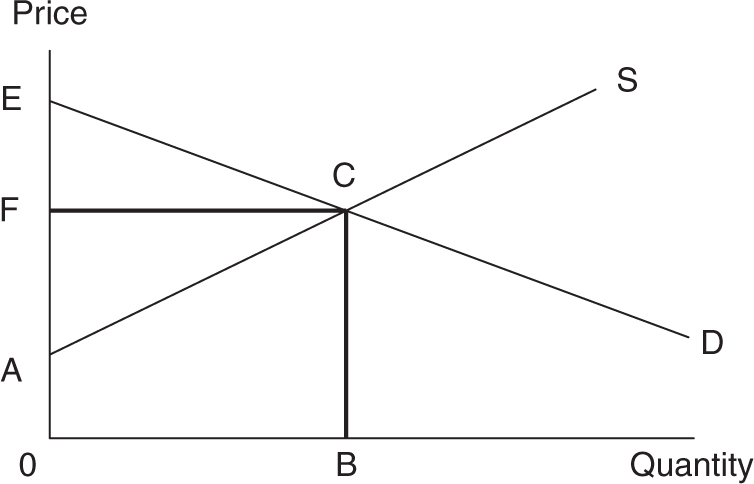

Figure D.2

7 . In Figure D.2 , identify the area of consumer surplus.

(A) 0ACB

(B) 0FCB

(C) AFC

(D) ACE

(E) FCE

8 . Suppose the price of beef rises by 10 percent and the quantity of beef demanded falls by 20 percent. We can conclude that

(A) demand for beef is price elastic and consumer spending on beef is falling.

(B) demand for beef is price elastic and consumer spending on beef is rising.

(C) demand for beef is price inelastic and consumer spending on beef is falling.

(D) demand for beef is price inelastic and consumer spending on beef is rising.

(E) demand for beef is unit elastic and consumer spending on beef is constant.

9 . If the price of firm A’s cell phone service rises by 5 percent and the quantity demanded for firm B’s cell phone service increases by 10 percent, we can say that

(A) demand for firm B is price elastic.

(B) supply for firm B is price elastic.

(C) firms A and B are substitutes because the cross-price elasticity is greater than zero.

(D) firms A and B are complements because the cross-price elasticity is less than zero.

(E) firms A and B are complements because the cross-price elasticity is greater than zero.

10 . Which of the following describes the theory behind the demand curve?

(A) Decreasing marginal utility as consumption rises.

(B) Increasing marginal cost as consumption rises.

(C) Decreasing marginal cost as consumption rises.

(D) Increasing total utility at an increasing rate as consumption rises.

(E) The substitution effect is larger than the income effect.

11 . If a consumer is not required to pay a monetary price for each cookie she consumes, the consumer will stop eating cookies when

(A) the total utility from eating cookies is equal to zero.

(B) the substitution effect outweighs the income effect from eating cookies.

(C) the ratio of marginal utility divided by total utility is equal to one.

(D) the marginal utility from eating the last cookie is zero.

(E) the marginal utility from eating the next cookie is increasing at a decreasing rate.

12 . In the short run, a firm employs labor and capital to produce gadgets. If the annual price of capital increases, what will happen to the short-run cost curves?

(A) The marginal cost and average variable cost curves will shift upward.

(B) The average fixed cost and average total cost curves will shift upward.

(C) The marginal cost and average fixed cost curves will shift upward.

(D) The marginal cost, average fixed cost, average variable cost, and average total cost curves will all shift upward.

(E) Only the average fixed cost curve will shift upward.

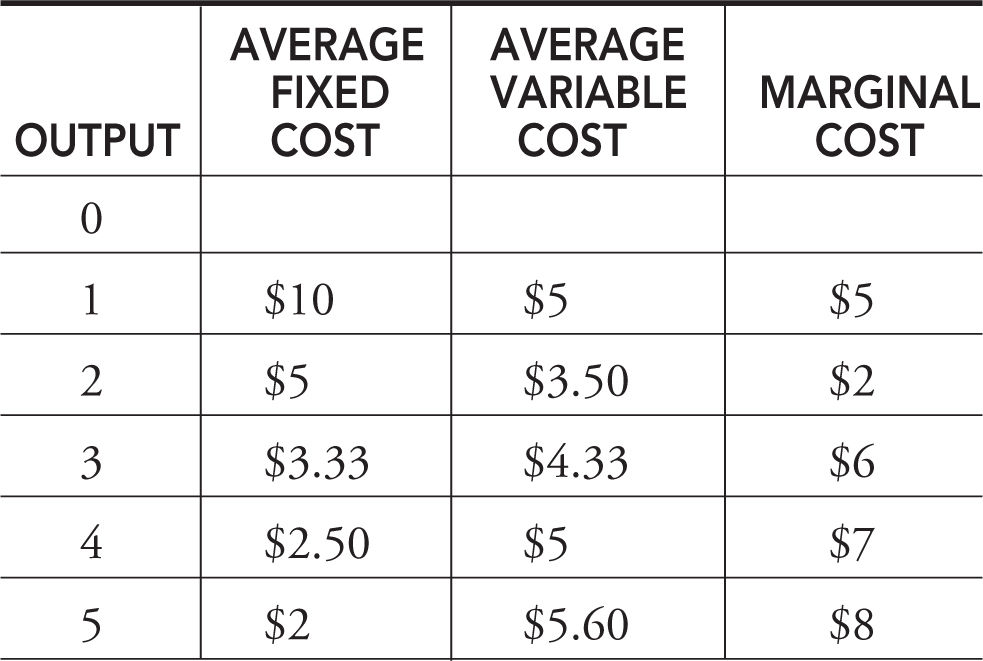

Questions 13 to 15 are based on the table of costs below for a perfectly competitive firm.

13 . The total fixed cost of producing a quantity of 4 is

(A) $5.

(B) $7.50.

(C) $7.

(D) $2.50.

(E) $10.

14 . The first unit of output to exhibit diminishing marginal productivity is the _____ unit.

(A) 1st

(B) 2nd

(C) 3rd

(D) 4th

(E) 5th

15 . At a quantity of 4, what is the total cost of production?

(A) $7.50

(B) $2.50

(C) $15

(D) $30

(E) $14.50

16 . Monopolistic competition is often characterized by

(A) strong barriers to entry.

(B) a long-run price that exceeds average total cost.

(C) a price that exceeds average variable cost, causing excess capacity.

(D) a homogenous product.

(E) many resources devoted to advertising.

Questions 17 to 18 are based on Figure D.3 , which illustrates the short-run cost curves of a perfectly competitive firm.

Figure D.3

17 . The shutdown point is seen at:

(A) P 0, q 0

(B) P 1, q 1

(C) P 2, q 2

(D) P 3, q 3

(E) P 3, q 4

18 . If the market price of the output increases from P 1 to P 3, the profit-maximizing firm will

(A) increase output from q 1 to q 4 and earn positive economic profits.

(B) increase output from q 1 to q 4 and earn a normal profit.

(C) increase output from q 1 to q 3 and earn positive economic profits.

(D) increase output from q 1 to q 3 and earn a normal profit.

(E) increase output from q 1 to q 2 and earn economic losses.

19 . If the perfectly competitive price is currently below minimum average total cost, we can expect which of the following events in the long run?

(A) The price will rise and each firm’s output will fall as firms exit the industry.

(B) Market equilibrium quantity will increase as firms exit the industry.

(C) Nothing. The industry is currently in long-run equilibrium.

(D) Profits will fall as the market price increases.

(E) The price will rise to the breakeven point as firms exit the industry.

20 . When a monopolist has maximized profit,

(A) price is set equal to marginal cost, creating zero economic profit.

(B) output is set where price is equal to average total cost.

(C) price is set above marginal cost, creating allocative inefficiency.

(D) any short-run profit will be eliminated through the long-run entry of new firms.

(E) output is set where price is equal to marginal cost, eliminating any deadweight loss.

21 . Which of the following is necessarily a characteristic of oligopoly?

(A) Free entry into and exit from the market

(B) A few large producers

(C) One producer of a good with no close substitutes

(D) A homogenous product

(E) No opportunities for collusion between firms

22 . The market structures of perfect competition and monopolistic competition share which of the following characteristics?

(A) Ease of entry and exit in the long run

(B) Homogenous products

(C) Perfectly elastic demand for the firm’s product

(D) Long-run positive profits

(E) Rigid or “sticky” prices

23 . If the government wishes to regulate a natural monopoly so that it produces an allocatively efficient level of output, it would be at an output

(A) where price is equal to average total cost.

(B) where marginal revenue equals marginal cost.

(C) where normal profits are made.

(D) where price is equal to average variable cost.

(E) where price is equal to marginal cost.

24 . Which of the following is most likely to decrease the demand for kindergarten teachers?

(A) An increase in funding for education

(B) Increased immigration of foreign citizens and their families

(C) A decrease in the average number of children per household

(D) Subsidies given to college students who major in elementary education

(E) A decrease in the number of classes the state requires for a teaching certificate

25 . Which of the following statements is true about the demand for labor?

(A) It rises if the price of a substitute resource falls and the output effect is greater than the substitution effect.

(B) It falls if the price of the output produced rises.

(C) It falls if the price of a complementary resource falls.

(D) It falls if the demand for the output produced by labor increases.

(E) It falls if the labor becomes more productive.

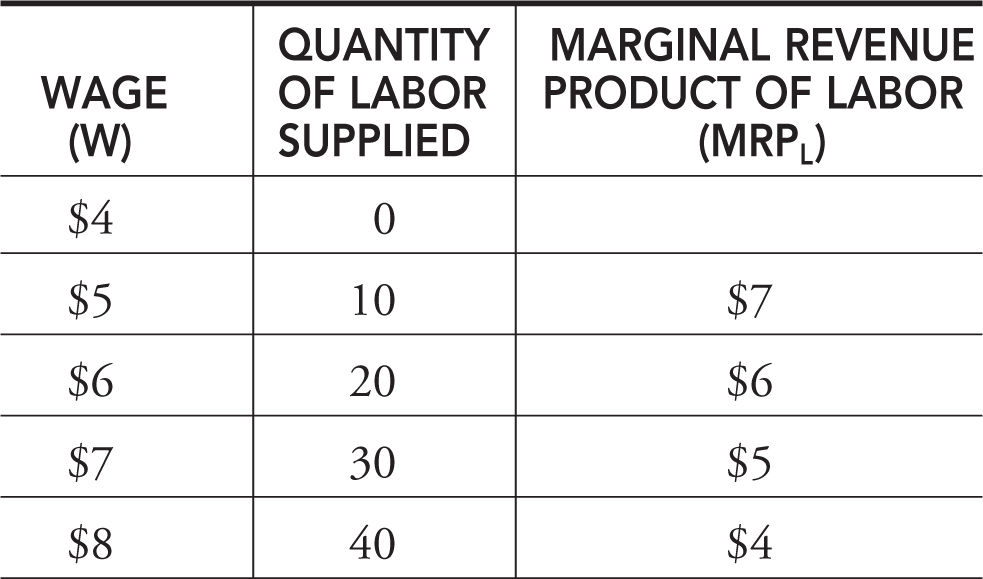

Questions 26 to 27 are based on the table of employment data below.

26 . If a firm is hiring labor in the perfectly competitive labor market, the wage and employment will be

(A) $4 and zero.

(B) $5 and 10.

(C) $6 and 20.

(D) $7 and 30.

(E) $8 and 40.

27 . If the above firm were a monopsonist, the wage would be _________ and employment would be _________ the competitive outcome.

(A) greater than; less than

(B) less than; greater than

(C) greater than; greater than

(D) less than; less than

(E) less than; the same as

28 . Which of the following is the best example of a public good?

(A) A visit to the orthodontist

(B) A session at the tanning salon

(C) A large pizza

(D) A cup of coffee

(E) The International Space Station

29 . A negative externality in the market for a good exists when

(A) the market overallocates resources to the production of this good.

(B) spillover benefits are received by society.

(C) the marginal social benefit equals the marginal social cost.

(D) total welfare is maximized.

(E) the marginal private cost exceeds the marginal social cost.

30 . Which of the following tax systems is designed to redistribute income from the wealthy to the poor?

(A) A progressive tax system

(B) A regressive tax system

(C) A proportional tax system

(D) An excise tax system

(E) A tariff system

Microeconomics Answers and Explanations, Section I

This diagnostic exam was designed to test you on topics that you will see on the AP Microeconomics exam in the approximate proportions that you will see them. Chronologically they appear in the approximate order of their review in Step 4 of this book, but this is not the case on the AP exam. Topics on the practice exams are shuffled.

Questions from Chapter 5

1 . C —This is the definition of scarcity.

2 . B —In a capitalistic market economy, the central government has minimal roles in the production and distribution of goods. Resources are allocated based on relative, not absolute, prices, and prices are determined in markets. The role of private property is central to capitalism.

3 . E —A concave, or bowed out, PPC illustrates the principle of increasing opportunity costs. It is more and more difficult (costly) to produce increasing amounts of a good.

Questions from Chapter 6

4 . B —In a market free of price controls or other distortions, equilibrium occurs at a price where Q d = Q s . Graphically this is where the demand curve intersects the supply curve. Here, social welfare is maximized, allocative efficiency is attained, and there exists no deadweight loss.

5 . D —If the price of a production input (or resource) increases, the supply curve shifts leftward and the price of gasoline rises. Hint: Having a strong grasp of what shifts supply and demand curves will really pay off. Draw these shifting curves in the margin of the exam book!

6 . A —Increased demand, by itself, increases equilibrium quantity and increases the price of grapes. Increased supply, by itself, increases equilibrium quantity and decreases the price of grapes. So quantity definitely increases, but the price change is unknown because it depends on how far the curves shift in relation to each other. Quickly draw these in the exam book.

7 . E —Consumer surplus is the area above the price and below the demand curve. It is the difference between the price consumers would have paid and the price they did pay.

Questions from Chapter 7

8 . A —If the percentage change in Q d is greater than the percentage change in price, the good is elastic. In this situation of rising prices, total spending on beef will fall because the upward effect of prices is outweighed by the downward effect of quantity.

9 . C —The cross-price elasticity measures how sensitive the Q d of good X is to a change in the price of good Y. If this elasticity is greater than zero, the two goods are substitutes, and if it is negative, the two goods are complements.

10 . A —One of the foundations of the law of demand is falling marginal utility as more of a good is consumed. You can eliminate any choices that refer to marginal cost, and a downward-sloping demand curve would not be the result of total utility that increases at an increasing rate.

11 . D —A consumer stops eating cookies when total utility is maximized, which corresponds to when MU = 0. Because marginal utility falls with consumption, the very next cookie will give the consumer disutility (MU < 0), so she stops.

Questions from Chapter 8

12 . B —An increase in the price of capital is an increase in total fixed costs. This increases AFC. Since ATC = AFC + AVC, it also increases ATC. Because fixed costs do not change with output, marginal cost and variable cost remain the same.

13 . E —TFC are constant, so if AFC = $10 at q = 1 and AFC = TFC/q , then TFC must be $10 at any quantity. Know the way in which all total and average costs are related.

14 . C —This question tests whether you know the relationships between production and cost. Marginal cost and marginal product are inverses of each other. Because the MC of producing the third unit is rising, the MP must be falling.

15 . D —At a quantity of 4, TFC = $10 and TVC = AVC × q = $5 × 4 = $20. Since TC = TFC + TVC, TC = $30.

Questions from Chapter 9

16 . E —Monopolistic competition is characterized by product differentiation. One way that firms differentiate their products and protect market share is through extensive advertising.

17 . B —The shutdown point is at minimum AVC. If the price falls below this point, the firm finds it rational to produce nothing in the short run and incur losses equal to TFC.

18 . C —When the price rises, the perfectly competitive firm finds a higher level of output where P = MR = MC. Since this price lies above the ATC curve, positive economic profits are possible.

19 . E —The question describes a situation where short-run losses are being incurred. In the long run, firms exit, shifting market supply leftward, increasing market price until the firms earn normal, or breakeven, profits.

20 . C —One of the important results of monopoly is that while output is set where MR = MC, price is set from the demand curve, so P > MC. This creates inefficient resource allocation and deadweight loss that is not eliminated in the long run.

21 . B —Oligopolies are industries dominated by a few large firms but can have either homogenous or differentiated products. All other choices describe other market structures in the chapter.

22 . A —These two market structures are fairly similar, and free entry and exit is one of the characteristics that they share. They also share the characteristic of normal profits in the long run but do not share homogenous products or efficiency.

23 . E —In perfect competition, P = MR = MC and resources are allocated efficiently. Since a monopoly will not have the situation where P = MR, regulators might try to force the firm to produce where P = MC. This point may or may not ensure a long-run profit for the firm.

Questions from Chapter 10

24 . C —Demand for any type of labor is derived from the demand for the good or service that the labor produces. With fewer children in the household, there will be less demand for kindergarten classes and teachers.

25 . A —When the price of a substitute resource (like capital) falls, two effects move the demand for labor in opposite directions. The firm wants to substitute for more capital and less labor, but lower costs prompt more output to be produced, and this can require more labor. If the output effect outweighs the substitution effect, demand for labor may increase even if capital is less expensive. Labor demand will increase if the labor becomes more productive or if the price of the output produced rises.

26 . C —Competitive labor markets are characterized by hiring where W = MRPL. This is another example of decision making where marginal costs (wage paid) equal marginal benefits (MR × MPL).

27 . D —A monopsonist is like a monopolist on the hiring side of the firm. Monopsonists hire where MFC = MRPL, and because MFC lies above the labor supply curve, this means that they will hire fewer workers and pay lower wages than the competitive outcome.

Questions from Chapter 11

28 . E —Public goods cannot be divided among consumers. If one consumes a public good, the next person is not denied consumption of it. All other choices are goods and services that are both rival and excludable.

29 . A —When individuals and firms exchange a good that imposes costs on third parties, they have created a negative externality. The market produces “too much” because these spillover costs are not reflected in the private (or market) supply curve. Resources are overallocated to the production of this good.

30 . A —A progressive tax system means that higher levels of income pay higher proportions of their income to the tax collector. This system is designed to redistribute income from higher tax brackets to lower tax brackets.

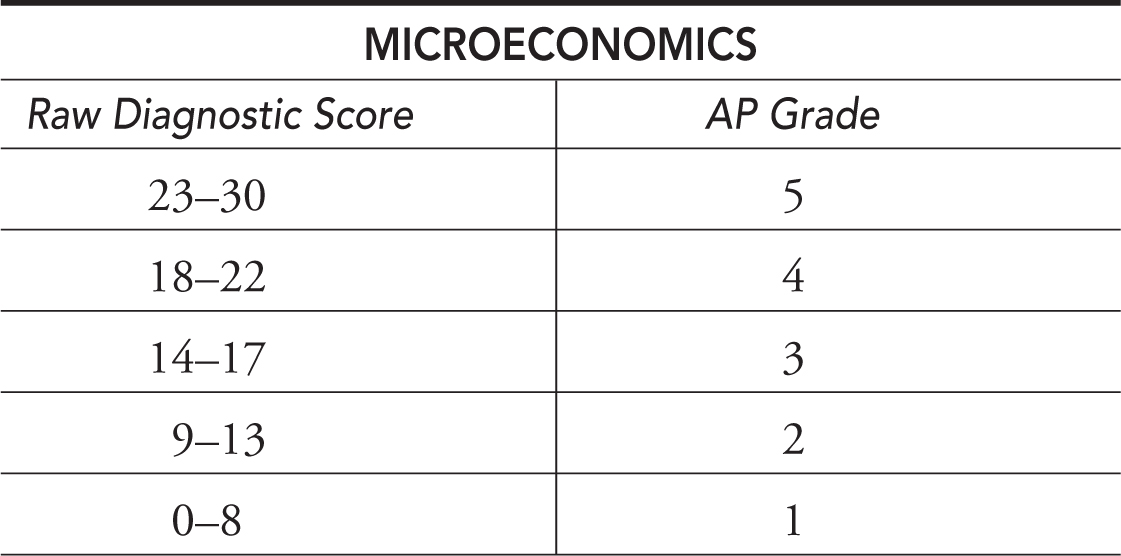

Scoring and Interpretation

Now that you have completed the diagnostic exam and checked your answers, it is time to assess your knowledge and preparation. If you saw some questions that caused you to roll your eyes and mutter “What the . . . ?” then you can focus your study on those areas. If you breezed through some questions, great!

Calculate your raw score with the formula that follows. If you left any questions blank, there is no penalty. Take this raw score on the diagnostic exam and compare it to the table that follows to estimate where you might score at this point.

Section I Raw Score = Nright

Remember, on the real exam, Section I will account for two-thirds of your composite score, with one-third coming from the free-response Section II. Given this important difference between your diagnostic exam and the real thing, the table is a very preliminary way to convert your diagnostic raw score to an AP grade. No matter how you scored on the diagnostic exam, it is time to begin to review for your AP Microeconomics exam.