Cracking the SAT with 5 Practice Tests, 2014 Edition (2013)

Paying For College 101

If you’re reading this book, you’ve already made an investment in your education. You may have shelled out some cold hard cash for this book, and you’ve definitely invested time in reading it. It’s probably even safe to say that this is one of the smaller investments you’ve made in your future so far. You put in the hours and hard work needed to keep up your GPA. You’ve paid test fees and application fees, perhaps even travel expenses. You have probably committed time and effort to a host of extracurricular activities to make sure colleges know that you’re a well-rounded student.

But after you get in, there’s one more issue to think about: How do you pay for college?

Let’s be honest: College is not cheap. The average tuition for a private four-year college is about $33,000 a year. The average tuition of a four-year public school is about $6,695 a year. And the cost is rising. Every year the sticker price of college education bumps up about 6 percent.

![]()

More Great Titles from

The Princeton Review

Paying for College Without

Going Broke

The Best 376 Colleges

Like many of us, your family may not have $33,000 sitting around in a shoebox. With such a hefty price tag, you might be wondering: “Is a college education really worth it?” The short answer: Yes! No question about it. A recent survey by the College Board showed that people with a college degree earn 60 percent more than people who enter the workforce with only a high school diploma. Despite its steep price tag, a college education ultimately pays for itself.

Still, the cost of college is no joke. It’s said that a college education ultimately pays for itself; however, some pay better than others. It’s best to be prudent when determining the amount of debt that is reasonable for you to take on.

Here’s the good news. Even in the wake of the current financial crisis, financial aid is available to almost any student who wants it. There is an estimated $177 billion—that’s right, billion!—in financial aid offered to students annually. This comes in the form of federal grants, scholarships, state-financed aid, loans, and other programs.

We know that financial aid can seem like an overwhelmingly complex issue, but the introductory information in this chapter should help you grasp what’s available and get you started in your search.

How Much Does College Really Cost?

When most people think about the price of a college education, they think of one thing and one thing alone: tuition. It’s time to get that notion out of your head. While tuition is a significant portion of the cost of a college education, you need to think of all the other things that factor into the final price tag.

Let’s break it down.

· Tuition and fees

· Room and board

· Books and supplies

· Personal expenses

· Travel expenses

Collectively, these things contribute to your total Cost of Attendance (COA) for one year at a college or university.

Understanding the distinction between tuition and COA is crucial because it will help you understand this simple equation:

![]()

Check out our Financial

Aid Library

PrincetonReview.com

When you begin the financial aid process, you will see this equation again and again. We’ve already talked about the COA, so let’s talk about the Estimated Family Contribution, or EFC. The EFC simply means, “How much you and your family can afford to pay for college.” Sounds obvious right?

Here’s the catch: What you think you can afford to pay for college, what the government thinks you can afford to pay for college, and what a college or university thinks you can afford to pay for college are, unfortunately, three different things. Keep that in mind as we discuss financing options later on.

The final term in the equation is self-explanatory. Anything that’s left after what you and your family have contributed, still needs to be covered. That’s where financial aid packages come in.

WHAT’S IN A FINANCIAL AID PACKAGE?

A typical financial aid package contains money—from the school, federal government, or state—in various forms: grants, scholarships, work-study programs, and loans.

Let’s look at the non-loan options first. Non-loan options include grants, scholarships, and work-study programs. The crucial thing about them is that they involve monetary assistance that you won’t be asked to pay back. They are as close as you’ll get to “free money.”

Grants

Grants are basically gifts. They are funds given to you by the federal government, state agencies, or individual colleges. They are usually need-based, and you are not required to pay them back.

One of the most important grants is the Pell Grant. Pell Grants are provided by the federal government but administered through individual schools. Amounts can change yearly. The maximum Federal Pell Grant award is $5,550 for the 2012–2013 award year (July 1, 2012 to June 30, 2013).

You apply for a Pell Grant by filling out the Free Application for Federal Student Aid (FAFSA). Remember that acronym because you’ll be seeing it again. Completing the FAFSA is the first step in applying for any federal aid. The FAFSA can be found online at www.fafsa.ed.gov.

There are several other major federal grant programs that hand out grants ranging from $100 to thousands annually. Some of these grants are given to students entering a specific field of study and others are need-based, but all of them amount to money that you never have to pay back. Check out the FAFSA website for complete information about qualifying and applying for government grants.

The federal government isn’t the only source of grant money. State governments and specific schools also offer grants. Use the Internet, your guidance counselor, and your library to see what non-federal grants you might be eligible for.

Believe It or Not…

The Chick and Sophie

Major Memorial Duck

Calling Contest, held

annually by the Chamber

of Commerce of Stuggart,

Arkansas, gives out

college scholarships

totaling $4,250 (as of

2011) to those high school

seniors who can master

hailing, feeding, comeback,

and mating duck calls.

Scholarships

Like grants, you never have to pay a scholarship back. But the requirements and terms of a scholarship might vary wildly. Most scholarships are merit- or need-based, but they can be based on almost anything. There are scholarships based on academic performance, athletic achievements, musical or artistic talent, religious affiliation, ethnicity, and so on.

When hunting for scholarships, one great place to start is the Department of Education’s free “Scholarship Search,” available at www.careerinfonet.org/scholarshipsearch. It includes over 5,000 scholarships, fellowships, loans, and other opportunities. It’s a free service and a great resource.

There is one important caveat about taking scholarship money. Some, but not all, schools think of scholarship money as income and will reduce the amount of aid they offer you accordingly. Know your school’s policy on scholarship awards.

Federal Work-Study (FWS)

One of the ways Uncle Sam disperses aid money is by subsidizing part-time jobs, usually on campus, for students who need financial aid. Because your school will administer the money, they get to decide what your work-study job will be. Work-study participants are paid by the hour, and federal law requires that they cannot be paid less than the federal minimum wage.

One of the benefits of a work-study program is that you get a paycheck just like you would at a normal job. The money is intended to go towards school expenses, but there are no controls over exactly how you spend it.

Colleges and universities determine how to administer work-study programs on their own campuses, so you must apply for a FWS at your school’s financial aid office.

The Bottom Line?

Not So Fast!

It is possible to appeal the

amount of the financial

aid package a school

awards you. To learn

more about how to do

that, check out “Appealing

Your Award Package” at

PrincetonReview.com/appealing-your-award.aspx

LOANS

Most likely, your entire COA won’t be covered by scholarships, grants, and work-study income. The next step in gathering the necessary funds is securing a loan. Broadly speaking, there are two routes to go: federal loans and private loans. Once upon a time, which route to choose might be open for debate. But these days the choice is clear: Always try to secure federal loans first. Almost without exception, federal loans provide unbeatable low fixed-interest rates; they come with generous repayment terms; and, although they have lending limits, these limits are quite generous and will take you a long way toward your goal. We’ll talk about the benefits of private loans later, but they really can’t measure up to what the government can provide.

Stafford Loans

The Stafford loan is the primary form of federal student loan. There are two kinds of Stafford loans: direct Stafford loans, which are administered by the Department of Education; and Federal Family Education Loans (FFEL), which are administered by a private lender bound by the terms the government sets for Stafford loans (FFEL loans are sometimes referred to as indirect Stafford loans, as well). Both direct and FFEL loans can be subsidized or unsubsidized. Students with demonstrated financial need may qualify for subsidized loans. This means that the government pays interest accumulated during the time the student is in school. Students with unsubsidized Stafford loans are responsible for the interest accumulated while in school. You can qualify for a subsidized Stafford loan, an unsubsidized Stafford loan, or a mixture of the two.

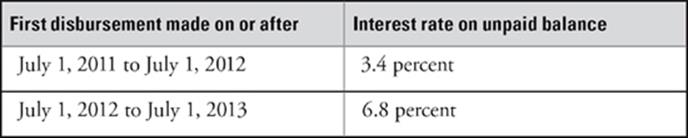

Stafford loans are available to all full-time students and most part-time students. Though the terms of the loan are based on demonstrated financial need, lack of need is not considered grounds for rejection. No payment is expected while the student is attending school. The interest rate on your Stafford loan will depend on when your first disbursement is. The chart below shows the fixed rates set by the government.

Finally, depending on the amount owed and the payment plan agreed upon by the borrower and lender, students have between 10 and 25 years to pay off their loan.

As with grants, you must start by completing the Free Application for Federal Student Aid (FAFSA) to apply for a Stafford loan.

PLUS Loans

Another important federal loan is the PLUS loan. This loan is designed to help parents and guardians put dependent students through college. Like the Stafford loan, a PLUS loan might be a direct loan from the government, administered by your school’s financial aid office, or it might be administered by a private lender who is bound to federal guidelines. Unlike the Stafford loan, the PLUS has no fixed limits or fixed interest rates. The annual limit on a PLUS loan is equal to your COA minus any other financial aid you are already receiving. It may be used on top of a Stafford loan. The interest rates on PLUS loans are variable though often comparable to, or even lower than, the interest rates on Stafford loans. Borrowers can choose when they will start paying the loan back: starting either 60 days from the first disbursement or six months after the dependent student has finished school.

To apply for a PLUS loan, your guardians must apply to the financial aid office of your school or with a FFEL private lender.

Perkins Loans

A third and final federal loan you should be aware of is the Perkins loan. Intended to help out students in extreme need, the Perkins loan is a government-subsidized loan that is administered only through college and university financial aid offices. Under the terms of a Perkins loan, you may borrow up to $5,500 a year of undergraduate study, up to $27,500. The Perkins loan has a fixed interest rate of just 5 percent. Payments against the loan don’t start until nine months after you graduate. Apply for Perkins loans through your school’s financial aid office.

Private Lenders

We said it before, and we’ll say it again: DO NOT get a private loan until you’ve exhausted all other options.

That said, there are some benefits to securing a private loan. First off, many students find that non-loan and federal loan options don’t end up covering the entire bill. If that’s the case, then private lenders might just save the day. Second, loans from private sources generally offer you greater flexibility with how you use the funds. Third, private loans can be taken out at anytime during your academic career. Unlike most non-loan and government-backed financial options, you can turn to private lenders whenever you need them.

All private lenders are not the same! As the old song says, “You better shop around.” Every lender is going to offer you a different package of terms. What you need to do is find the package that best fits your needs and plans. Aside from low interest rates, which are crucially important, there are other terms and conditions you will want to look out for.

Low origination fees Origination fees are fees that lenders charge you for taking out a loan. Usually the fee is simply deducted automatically from your loan checks. Obviously, the lower the origination fee, the better.

Minimal guaranty fees A guaranty fee is an amount you pay to a third-party who agrees to insure your loan. That way, if the borrower—that is you—can’t pay the loan back, the guarantor steps in and pays the difference. Again, if you can minimize or eliminate this fee, all the better.

Interest rate reductions Some lenders will reduce your interest rates if you’re reliable with your payments. Some will even agree to knock a little off the interest rate if you agree to pay your loans through a direct deposit system. When shopping for the best loan, pay careful attention to factors that might help you curb your interest rates.

Flexible payment plans One of the great things about most federal loans is the fact that you don’t have to start paying them off until you leave school. In order to compete, many private lenders have been forced to adopt similarly flexible payment plans. Before saying yes to a private loan, make sure that it comes with a payment timetable you can live with.

WHERE THERE’S A WILL THERE’S A WAY

No matter what the state of the economy, going to college will always make good financial sense. This is especially true today, with the wealth of low-interest federal assistance programs available to you. There are plenty of excellent financing options out there. With a little effort (and a lot of form-filling!) you’ll be able to pay your way through school without breaking the bank.